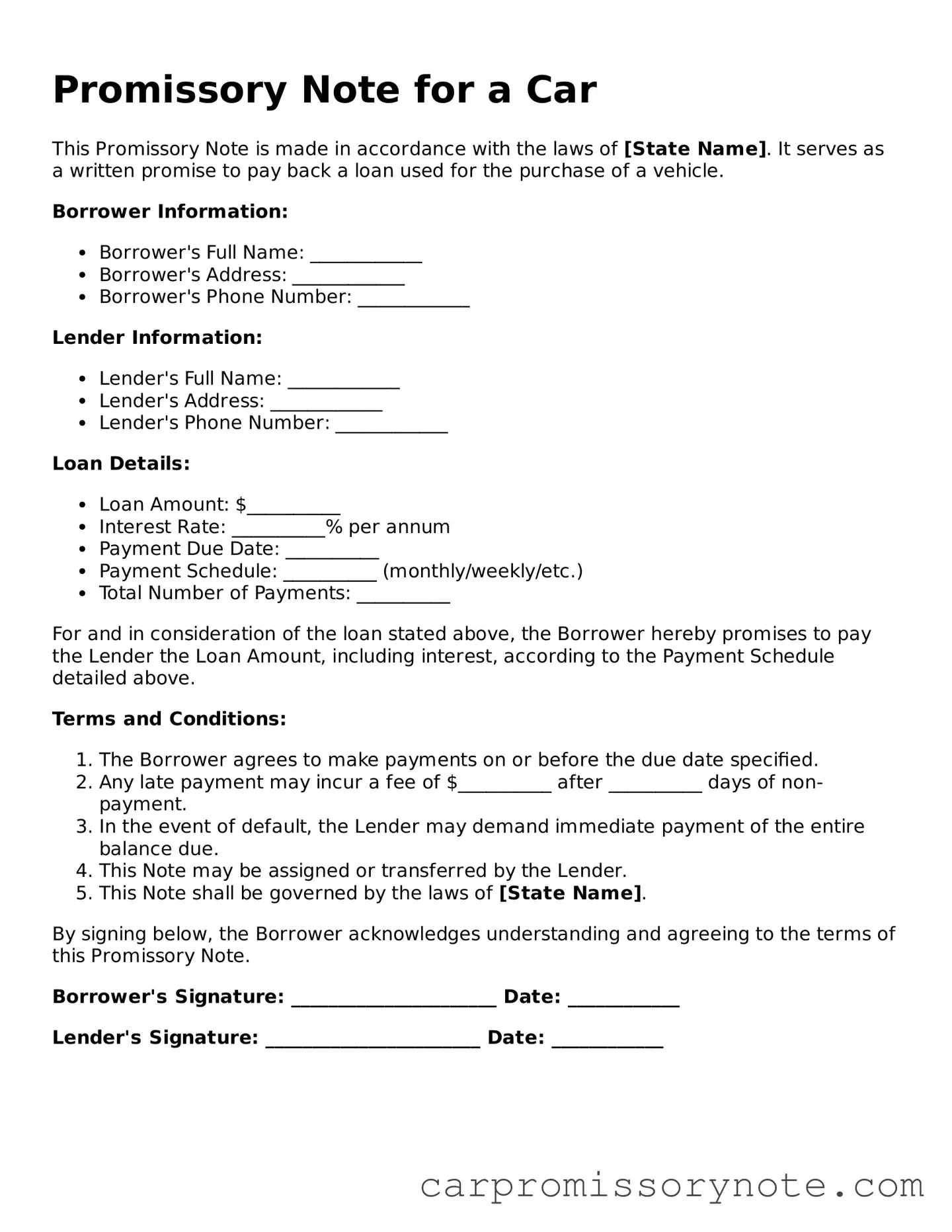

When purchasing a vehicle, many buyers find themselves navigating the complexities of financing options. A Promissory Note for a Car serves as a critical document in this process, outlining the agreement between the buyer and the lender regarding the repayment of the loan. This form typically includes essential details such as the loan amount, interest rate, repayment schedule, and the consequences of default. By clearly stating the terms of the loan, the Promissory Note protects both parties involved. It ensures that the buyer understands their financial obligations while providing the lender with a legal recourse in case of non-payment. Additionally, this document may also specify the collateral involved, often the vehicle itself, which secures the loan. Understanding the nuances of this form is crucial for anyone looking to finance a car, as it lays the foundation for a transparent and fair transaction.

When dealing with a Promissory Note for a Car, understanding the key elements is crucial for both the lender and the borrower. Here are some important takeaways:

By following these guidelines, both the lender and borrower can navigate the process smoothly and maintain a clear understanding of their financial obligations.

| Fact Name | Description |

|---|---|

| Definition | A promissory note for a car is a written promise to pay a specified amount of money for the purchase of a vehicle. |

| Parties Involved | The note typically involves two parties: the borrower (buyer) and the lender (seller or financial institution). |

| Governing Law | The laws governing promissory notes vary by state. For example, in California, the Uniform Commercial Code (UCC) applies. |

| Payment Terms | The note outlines specific payment terms, including the total amount, interest rate, and payment schedule. |

| Default Conditions | Conditions under which the borrower defaults are typically included, detailing the lender's rights in such cases. |

| Transferability | Promissory notes can often be transferred to another party, which may affect the rights and obligations of the original parties. |

| Signatures Required | Both parties must sign the promissory note for it to be legally binding. |

| State-Specific Forms | Some states may have specific forms or requirements for promissory notes, so it’s important to check local regulations. |

Filling out a Promissory Note for a Car can seem straightforward, but many people make common mistakes that can lead to issues down the road. One frequent error is not providing accurate information about the borrower and lender. It’s essential to include the correct names and addresses. If there’s a mistake, it could complicate communication or even lead to legal disputes later.

Another mistake often made is failing to clearly state the loan amount. Some individuals may overlook this detail or write it down incorrectly. A vague or incorrect loan amount can create confusion regarding repayment terms. It’s crucial to double-check this figure to ensure that both parties are on the same page.

Additionally, people sometimes neglect to specify the interest rate or repayment schedule. Without these details, the agreement lacks clarity. This can lead to misunderstandings about how much needs to be paid back and when. Always ensure that both the interest rate and the payment schedule are clearly outlined in the document.

Lastly, forgetting to sign the document is a common oversight. A Promissory Note is not valid without signatures from both the borrower and the lender. This step is vital, as it shows that both parties agree to the terms laid out in the note. Always remember to review the document one last time to ensure all signatures are in place.

A loan agreement is similar to a promissory note for a car in that both documents outline the terms of borrowing money. In a loan agreement, the lender and borrower agree on the loan amount, interest rate, and repayment schedule. The loan agreement may also include details about collateral, which protects the lender if the borrower defaults. Like a promissory note, it serves as a legal contract that binds both parties to the agreed terms.

A lease agreement shares similarities with a promissory note for a car, particularly in the context of vehicle leasing. In both cases, one party (the lessor or lender) allows another party (the lessee or borrower) to use the vehicle in exchange for payments. The lease agreement specifies the duration of the lease, monthly payments, and conditions for vehicle return. Both documents establish clear expectations and responsibilities for each party involved.

A mortgage is another document that resembles a promissory note, especially in how it secures a loan with collateral. When someone takes out a mortgage, they agree to repay the loan amount over time, much like a car loan. The property being purchased serves as collateral, meaning the lender can take possession if the borrower fails to make payments. Both documents detail the obligations of the borrower and the rights of the lender, ensuring clarity in the financial arrangement.

Understanding various financial documents is crucial for effective money management. For instance, the Ohio IT AR form serves an important purpose in the tax landscape, allowing individuals to request a refund of overpaid taxes after submitting their income tax returns. Accurate completion of this form is essential for anyone looking to reclaim funds. For further assistance with these forms, you can visit Ohio PDF Forms, which provide valuable resources for taxpayers.

An installment agreement is also akin to a promissory note for a car, as it involves a borrower making regular payments over time. In this case, the borrower agrees to pay a specific amount at set intervals until the debt is paid off. This document outlines the payment schedule, interest rates, and any penalties for late payments. Like a promissory note, it creates a clear framework for repayment, helping both parties understand their commitments.

When filling out the Promissory Note for a Car form, it's crucial to ensure accuracy and clarity. Below are some important dos and don'ts to consider:

Following these guidelines can help prevent misunderstandings and legal issues down the line. It's important to take this process seriously to protect all parties involved.

What is a Promissory Note for a Car?

A Promissory Note for a Car is a legal document that outlines the agreement between a borrower and a lender regarding the financing of a vehicle. Essentially, it serves as a written promise from the borrower to repay the loan amount, typically including details such as the interest rate, payment schedule, and any penalties for late payments. This note protects both parties by clearly stating the terms of the loan, ensuring that everyone understands their responsibilities.

What information do I need to include in the Promissory Note?

When creating a Promissory Note for a Car, it’s important to include specific information to make the document clear and enforceable. Key details should include the names and addresses of both the borrower and lender, the total loan amount, the interest rate, the payment schedule (including due dates), and the consequences of defaulting on the loan. Additionally, specifying whether the loan is secured or unsecured can provide further clarity. This ensures both parties are on the same page and helps prevent misunderstandings.

What happens if I default on the Promissory Note?

Defaulting on a Promissory Note means failing to make payments as agreed. If this occurs, the lender has the right to take specific actions outlined in the note. This may include charging late fees, accelerating the loan (demanding full payment immediately), or even repossessing the vehicle if the loan is secured by the car. It’s crucial to communicate with the lender if you anticipate difficulties in making payments. Many lenders are willing to work out alternative arrangements to help borrowers avoid default.

Can I modify the terms of the Promissory Note after it has been signed?

Yes, it is possible to modify the terms of a Promissory Note, but both parties must agree to the changes. This typically involves creating an amendment to the original note, which should be signed and dated by both the borrower and lender. It’s important to document any modifications in writing to ensure clarity and enforceability. Open communication is key, as both parties should feel comfortable discussing any necessary adjustments to the agreement.